Standard 0: Measurable Impact, Not Capital Deployed.

Success for MOFI’s Real Estate Investment Fund won’t be judged by how much capital is deployed-but by whether it delivers real, wealth-building homeownership for Nigerians.

EFIs must move from thinking like lenders to acting like fiduciaries, focused on helping households do better than renting. That is the only benchmark that matters.

In this first edition of The Boldmen Standards, we anchor the conversation where it should be-on outcomes, not optics.

Introduction

Homeownership has long been considered an important goal for many individuals in advanced economies. Beyond providing shelter, it is widely viewed as a key investment vehicle for personal wealth accumulation. However, for many Nigerians today, the decision to rent or own is determined purely by affordability. As homeownership is still seen more as a means of securing shelter and less as a vehicle for wealth accumulation, the rental market has simultaneously expanded to accommodate those who cannot afford to make outright home purchases. This interplay between renting and buying has far-reaching implications, influencing everything from the market rental prices to property values. Understanding the push-and-pull between these two housing options is essential, especially in the context of programs like the Ministry of Finance Incorporated Real Estate Investment Fund (MREIF), which must compete directly with the rental market to attract potential homeowners.

This analysis evaluates the MREIF initiative through the lens of the end-user–prospective homeowners–by examining the decision to rent or purchase a comparable property financed through participating financial institutions under the program. While considerable attention has been given to supporting the supply side–particularly via off-take guarantees and development finance–the long-term viability of MREIF ultimately depends on how effectively it enables commercial and mortgage banks to offer accessible, affordable mortgage products to individual buyers.

It is important to note that, the Ministry of Finance Incorporated itself does not issue mortgages directly to homebuyers. Instead, it has provided the capital base (via the Real Estate Investment Fund) that enables eligible financial institutions (EFIs) to extend mortgage loans at a fixed rate of 12% per annum, without relying on their shareholder funds. This funding mechanism is designed to enhance liquidity and stability in the mortgage market, making homeownership more attainable for first-time buyers.

Understanding the financial trade-offs faced by prospective homeowners–including the cost of ownership versus renting–offers a clearer view into the program’s effectiveness. Ultimately, the success of MREIF hinges not just on the flow of capital to lenders, but on whether the mortgage products offered through these institutions genuinely meet the financial needs and aspirations of the Nigerian household.

Even with a well-structured housing supply, sustaining demand requires careful consideration. What factors would incentivize a renter to transition to homeownership under MREIF? How does the program compare to the flexibility and lower upfront costs associated with renting? More critically, does it present a financially compelling and sustainable path to long-term wealth accumulation and housing stability?

This analysis will explore the key factors influencing renters’ decisions and employ a Rent vs. Own scenario analysis to assess the financial trade-offs involved. By examining these dynamics, EFIs can more effectively structure their mortgage finance offerings under the MREIF framework to align with the needs and incentives of prospective homeowners, ensuring the program delivers meaningful long-term benefits.

FAQS about the MREIF

It is important for readers to know why the MREIF program was launched, However, rather than delving into the subtleties here, readers are encouraged to visit the MREIF website, as well as that of the fund managers, ARM, who also provide a comprehensive overview. For readers seeking a bit of background and historical context, Mr. Adetola Akinsulire’s article, offers valuable insights into the program’s origins and objectives.

Key Considerations for First-Time Homebuyers–Addressing Critical Concerns to Strengthen the Appeal of Ownership Under MREIF Over Renting

In an economy where inflation erodes purchasing power and job security is uncertain, the average renter is not irrational–they’re cautious. For EFIs to be relevant, they must not only provide mortgages; they must offer a better deal than rent. That means addressing:

Upfront Cost Disparities: Renters pay their rent and walk in. Mortgage buyers face equity requirements, legal fees, valuation fees, and titling delays. EFIs must innovate around down payments–shared equity, government guarantees, or risk-based pricing–not just quote rates.

Liquidity and Exit Options: Homeowners are often trapped in illiquid markets. Renting offers mobility. Can EFIs develop mechanisms for refinancing, resale, or buy-back programs that preserve optionality?

Real Rate of Return: Homeownership must yield a return–either via capital appreciation or rent-equivalent savings. If house prices stagnate or servicing costs exceed imputed rent, the asset becomes a liability.

1. Mortgage Transferability & Assumability

One of the most underappreciated frictions in mortgage finance is illiquidity—the inability of a homeowner to efficiently exit a mortgage contract without forfeiting value. This problem is particularly acute in emerging markets like Nigeria, where income volatility and job mobility are real and growing. While renting is often dismissed as “throwing money away,” it does offer something ownership under MREIF currently struggles to replicate: flexibility. In a rental arrangement, a tenant can vacate on short notice with negligible financial consequences. In contrast, the homebuyer under a 20-year mortgage faces a long-duration obligation, irrespective of life events—relocation, employment shocks, or changing family needs. Unless this rigidity is resolved, the market will continue to reward flexibility over ownership. Rational households will choose liquidity over leverage.

For MREIF to offer a financially superior alternative to renting, it must enable homeowners to exit gracefully. This requires that mortgage instruments issued through (EFIs incorporate two key design features:

Mortgage Assumability: allowing qualified buyers to take over the remaining mortgage obligation on the same terms, without triggering a full refinancing event. The seller can thus exit without disrupting the capital structure of the transaction.

Equity Realization: If the property has appreciated, the seller must be able to monetize the difference between the market value and the outstanding mortgage balance. This equity gain is a critical part of the homeownership value proposition.

Without these mechanisms, the mortgage becomes economically inert. It traps the owner in a fixed position with no exit path, undermining one of the few advantages ownership should have over renting: the ability to build and extract equity.

Why This Matters

In theory, homeownership creates wealth. In practice, it only does so if the asset is liquid, tradable, and priced fairly. When these conditions fail, homeownership becomes a liability, not an asset. If EFIs under MREIF issue mortgages that cannot be transferred, they effectively penalize mobility, discourage uptake among young or middle-income earners, destroy the potential for wealth compounding through equity rollovers into future housing upgrades.

The policy irony is glaring: the same demographic the program seeks to assist–first-time buyers–is also the most likely to require geographic or financial mobility.

Critical Questions EFIs Must Address:

- Can MREIF-backed mortgages be assumed by qualified third parties without full refinancing? If not, liquidity is impaired.

- Can the seller realize the full market value of their equity gain upon resale? If not, wealth creation is stunted.

If the answer to either question is “no,” then renting remains the rational choice—and MREIF, however well-funded, cannot fulfill its mandate.

The term “sale”, “selling”, “resale” or “reselling” is used here in a technical sense, as it is not an outright sale but rather an assumption, by another qualified borrower, of the existing obligations of the homeowner under the mortgage. This distinction is crucial because an outright sale would trigger capital gains tax, whereas an assumption allows the homeowner to extract only the appreciated equity in the home, which is lower than the net profit from a full sale.

2. Prepayment Flexibility

A critical feature of any well-structured mortgage program is the ability of homeowners to accelerate repayment without undue penalties. Many homeowners may seek to pay off their mortgage early if they experience a windfall–whether through an inheritance, investment gains, or increased earnings. The ability to eliminate debt ahead of schedule not only provides financial security but also results in substantial interest savings over the life of the loan.

Yet if EFIs under the MREIF framework impose significant prepayment penalties, they introduce a distortion. The borrower is punished for acting responsibly. The net result: homeowners are trapped in long-term, interest-heavy loan contracts despite having the capacity to exit.

This not only undermines borrower trust but materially reduces the net present value (NPV) of homeownership relative to renting, where exit and reallocation of funds are frictionless.

To align with the broader MREIF mandate of encouraging affordable, flexible homeownership, prepayments should be penalty-free, especially after a minimum lock-in period (e.g., 24 months). Alternatively, penalties should be nominal and structured on a declining scale—e.g., 2% in Year 1, 1% in Year 2, and 0% thereafter.

Key Questions EFIs Must Address:

- Can homeowners pay off their mortgage early without penalties?

- What is the structure and rationale behind any prepayment fees imposed?

- Are they tied to actual losses incurred by the lender, or are they merely punitive?

Unless these questions are answered in a way that respects borrower flexibility, the program’s attractiveness relative to renting is compromised.

Credit: pexels.com

3. Hidden Fees

In the mortgage market, what you don’t know will cost you. For many first-time buyers, particularly those without a deep financial background, the apparent affordability of homeownership under the MREIF program begins and ends with the monthly mortgage payment. This is a dangerously incomplete picture. The true cost of homeownership is broader, more complex, and often concealed behind layers of transaction and post-transaction charges. This is why EFIs must adopt a full-cost disclosure standard that captures not just principal and interest, but every recurring and non-recurring obligation tied to the mortgage product.

A mortgage product that advertises a competitive interest rate but burdens the borrower with layered fees is not affordable–it is misleading. These “hidden” costs include:

- Upfront charges: Legal fees, valuation, underwriting, title registration, and processing fees.

- Recurring costs: Mortgage servicing fees, mandatory hazard insurance premiums, property taxes (where applicable).

- Post-acquisition obligations: Repairs, maintenance, and estate dues.

When aggregated, these costs significantly alter the borrower’s cash flow profile. A home that once appeared “affordable” on paper can quickly become a source of financial stress when real expenses exceed expectations.

Meanwhile, renting offers a key financial advantage: cost certainty. Monthly rent is typically a single line item. The landlord bears the cost of repairs, insurance, and property upkeep. In contrast, the homeowner assumes full exposure to both fixed and variable obligations.

This comparison matters. For EFIs to truly promote sustainable homeownership, they must quantify and disclose the total cost of ownership, including estimated maintenance–so that borrowers can rationally compare the financial profile of owning versus renting.

It becomes imperative for EFIs to adopt a standardized, itemized cost disclosure format, preferably with a pre-closing “total monthly housing expense” worksheet, so borrowers can understand their actual commitment in advance. In housing finance, truth builds trust. If the EFIs seeks to position homeownership as a pathway to long-term stability and wealth creation, it must first pass the test of transparency.

Key Questions EFIs Must Address:

- What is the effective cost (APR) of the MREIF mortgage program, including all additional fees? (Not just the nominal interest rate, but the true borrowing cost after factoring in all fees, insurance premiums, and loan servicing charges).

- Who bears the cost of hazard insurance, and is it escrowed into monthly payments or billed separately?

- Are borrowers responsible for all maintenance? If so, is a maintenance reserve recommended or required?

- When all components are included, does monthly housing cost under MREIF exceed average rent for similar properties?

Transparency is not merely a consumer protection feature–it is a strategic design imperative. Borrowers who discover unexpected costs after closing will erode trust in the program and may dissuade others from participating. At scale, this erodes the credibility of the entire mortgage framework.

Renting vs. Owning under MREIF

As stated earlier, an important consideration when analyzing the demand for home ownership investment is the cost of renting. If users find that renting is more cost-effective than owning, homeownership may not always be a better investment.

What follows is a comparative scenario analysis of the relative costs of owning a home under MREIF versus renting the same residence, given certain assumptions. The goal of this exercise is to compile all cash flows associated with each form of occupancy, and then calculate the rate of return that will be earned on the funds used to make an equity investment (down payment) if the home is purchased under the MREIF program. Alternatively, it is this rate of return that an individual would have to earn on the “down payment” saved if renting is chosen, to make renting the financial equivalent of owning.

By modeling multiple future scenarios and adjusting key variables such as the initial rent, down payment, appraised property value, expenses, interest rates, property growth rate, rental growth rate, and investment returns, we can assess the financial trade-offs between renting and owning. This will help ascertain the conditions under which homeownership under MREIF will become financially equivalent to, or more advantageous than, renting the same property. The analysis seeks to provide insights into the long-term financial implications of each choice, offering a data-driven approach to making an informed housing decision.

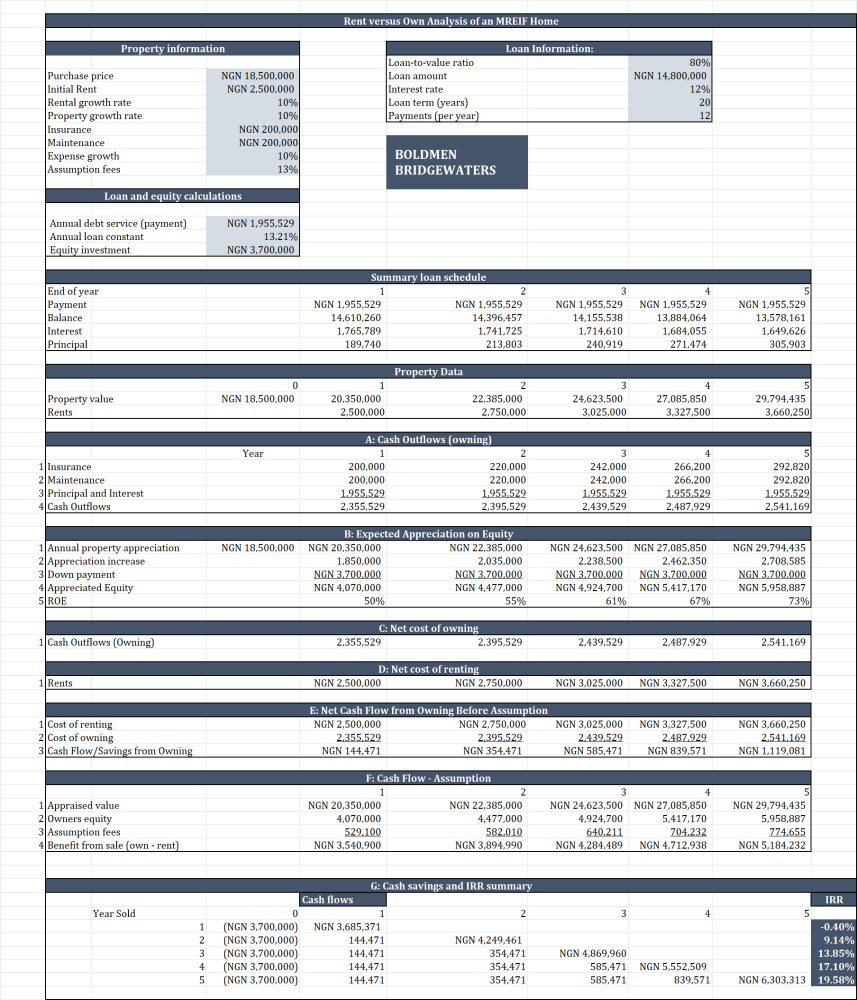

The analysis is modeled on the following assumptions:

- Property Value: N18,500,000

- Rent: N2,500,000

- Interest Rate: 12% (fixed)

- Term: 20 years

- Payments (per year): 12

- Loan-to-value ratio: 80% (20% down payment).

- Loan Assumption: Allowed–New qualified buyers can take over the existing mortgage.

- Property Growth Rate: 10% per year.

- Rental Growth Rate: 10% per year.

- Exit Strategy: Transfer existing obligations to a new qualified buyer after 5 years.

- Insurance: N200,000

- Maintenance: N200,000

- Expense Growth Rate: 10% per year.

- Assumption fees: 13% of appreciated equity.

Renting is superior if: FV of invested down payment + savings from lower monthly rent > Equity at sale (incl. capital gains from homeownership).

Owning is superior if: IRR on equity investment (down payment) from home purchase (via appreciation and savings from lower mortgage payments relative to rent) > return available from investing saved capital in alternative assets of comparable risk profiles.

Rent vs. Own Analysis

The framework for making a comparison between renting and owning under MREIF is presented in the analysis. In this example, we have a 2-bedroom terrace bungalow in New Karu, Nasarawa State that could be rented for N2,500,000 per year (N208,333 per month) or purchased under the MREIF program for N18,500,000 with N3,700,000 down and financed with a fully amortizing mortgage loan of N14,800,000 at a 12% interest for 20 years. Other costs associated with owning include maintenance expenses and insurance. In our example, these expenses would not have to be paid if renting is chosen. All other expenses would have to be paid regardless of whether the property is owned or rented, such as utilities–like electricity bills, security levies, and so on. Because they offset, they do not have to be included in our analysis. Other assumptions include (i) escalation in expenses, (ii) rents, (iii) property value at 10% per year, and (iv) 5 year period of analysis, at the end of which, the property would be “sold” via assumption. Assumption fees of 13% would have to be paid at that time.

Cash flows are summarized annually for convenience and presented in the analysis. Note that in panel A, we have summarized cash outflows associated with owning. The total cost of owning in year 1 is N2,355,529. The MREIF homeowner pays N162,960.75 per month for the mortgage, totaling N1,955,529 per year, in addition to the cost of insurance and maintenance at N200,000 each. If the property is owned, this means that rent of N2,500,000 does not have to be paid. To complete the annual outflow in the analysis, we must consider rent savings if owning is chosen. This amounts to N2,500,000 the first year and when included in the analysis produces a net savings from home ownership of N144,471, as shown in panel E. Note that savings in year 2 are N354,471 and so on. This analysis must be carried out each year to assess the net effects of increasing expenses such as maintenance, insurance, and increasing rents.

Finally, we must consider the proceeds from a “sale” (via assumption) of the mortgage. We calculate this for each year in panel F. The owner’s benefit in panel F is simply the appreciated equity, less assumption fees. The annual cash flows up to the year of “sale” and the cash flows produced from “sale” are combined, and internal rates of return are calculated and presented in panel G. Note that if the property is “sold” at the end of year 1, the IRR on the N3,700,000 investment would be negative. This means that if the property is expected to be sold after only one year, renting may be the wiser choice. However, returns from ownership improve in years 2 through 5, as the annual cash flows and the property value increase. The IRRs during those years indicate that to justify renting, an investor would have to earn from 9.14% to 19.6% on other investments equal in risk with the N3,700,000 equity saved to make renting equivalent to owning under MREIF.

Evaluating Future Decisions After Assumption

While the previous analysis presents a compelling framework for evaluating the costs and benefits of renting versus owning a home under the MREIF, further strategic questions emerge once the 5-year holding period ends. Specifically:

- What becomes of the proceeds from the assumed “sale” at year 5?

- Does the homeowner re-enter the rental market or continue as an owner?

- What if the owner opts not to sell at year 5, choosing instead to remain in the property indefinitely?

These are not merely theoretical questions–they are essential to forming a complete view of long-term housing strategy under MREIF and making informed investment decisions.

If the property is indeed sold at the end of year 5, the immediate question becomes: What next?

Because housing is a non-discretionary need, the owner must reallocate the sale proceeds either toward:

- Acquiring another home (triggering new ownership costs, likely at higher prices), or

- Entering the rental market, thus beginning to incur rental payments once again.

In essence, the sale at year 5 merely defers–but does not eliminate–the need for shelter-related outflows. Therefore, a robust investment strategy must contemplate not only the net proceeds from the sale but also their opportunity cost–i.e., what alternative housing expenses will be incurred, and how the proceeds will be reinvested or consumed.

Also, the decision to sell at the 5-year mark is not automatic. It depends critically on the owner’s life circumstances and local market trends.

– High Mobility Scenarios

If employment volatility, relocation, or lifestyle transitions are anticipated, the homeowner is more likely to exit the property earlier. In such cases, short-term ownership becomes less economically defensible–especially if transaction costs (e.g., assumption fees at 13%) are high. Unless property appreciation or rental inflation is significantly robust, short-term holding periods dilute the advantages of ownership. Renting, by contrast, offers flexibility and cost-efficiency under these conditions.

– Stable Tenure in High-Growth Markets

Conversely, if the homeowner expects to remain in the property for a longer term and if the location exhibits sustained property value appreciation (e.g., 10% annually as assumed), the economics of ownership become materially more attractive. In such environments, homeowners can:

- Amortize transaction costs over time

- Capture compounding equity gains

- Avoid escalating rental outflows

Thus, homeownership outperforms when the investment horizon aligns with market momentum.

Again, should the homeowner choose not to sell at year 5, but instead retain the property into the indefinite future, the analysis must transition from a discrete 5-year framework to a long-dated cash flow model. Several important factors come into play:

- Mortgage payments remain fixed, but rental prices likely continue rising.

- Maintenance and insurance expenses may increase, but are generally outpaced by rent inflation in growth markets.

- Equity accumulates steadily, reducing the effective cost of ownership over time.

- Appreciation-driven capital gains compound, enhancing total return on investment.

In this extended-hold scenario, the net present value (NPV) of homeownership continues to increase, while the marginal cost of renting escalates. Put differently, owning becomes increasingly efficient with time, especially in inflationary or high-demand markets.

Despite the structural advantages of long-term ownership, several economic scenarios may tilt the balance back in favor of renting:

- Rental Deflation: If rents begin to fall due to oversupply, economic downturn, or migration patterns, the comparative savings from ownership shrink.

- Rising Ownership Costs: Unexpected surges in insurance, maintenance, or regulatory costs may erode ownership’s appeal.

- Elevated Interest Rates: If future mortgage rates materially exceed the current 12% baseline, the upfront affordability and total cost of ownership would increase, particularly for new entrants.

In such cases, renting becomes a rational hedge against market and policy volatility.

A review of the five-year comparative cash flows (Panels B.1 and E.3) highlights two core drivers of homeownership advantage:

- Rent avoidance as a recurring cash flow benefit

- Equity appreciation as a capital accumulation mechanism

Both effects compound over time, increasing the internal rate of return (IRR) on the initial equity investment (N3.7 million). Therefore, if the holding period extends beyond 5 years, and if appreciation and rent inflation trends persist, ownership under MREIF can be expected to generate superior total returns compared to renting.

Reasons Why Renting Might Still Be Preferred

- For individuals who move often due to job changes, family needs, or personal reasons, renting provides greater flexibility than owning.

- Homeownership comes with risks, such as declining home values. Some people may not want to deal with market fluctuations.

- A desire to shift maintenance, security, and management to others.

- Housing markets sometimes experience bubbles, where prices rise unsustainably and then crash. Some people avoid buying to protect themselves from losses. This may occur when house prices rise relative to rents to such an extent that the prospect of further appreciation in prices becomes problematic.

To the extent that any or all of the above considerations are important to residents, they may be willing to forgo returns available from homeowning under MREIF and pay an implicit premium or opportunity cost to maintain renter status.

Credit: KindelMedia | pexels.com

Recommendations

- To accommodate the homeowner’s need for flexibility and to enhance the long-term benefits and sustainability of homeownership under MREIF, the EFIs should incorporate a structured pathway that allows first-time buyers to transition smoothly from their first home to a larger residence as their needs evolve. Given that many homeowners may choose to sell after five years–often due to family expansion, marriage, career changes, or the need for more space–EFIs should provide a framework that enables them to leverage the equity built in their initial home as a stepping stone to a larger property. Under this structure, homeowners who have accumulated equity in their first residence, growing from N3.7 million to approximately N5.18 million over five years, should be able to use this equity as a down payment on a bigger home within the MREIF system. Of course, this assumes that the household income has increased sufficiently to support the higher monthly housing obligations associated with a larger property.

- The Ministry of Finance Incorporated/EFIs should advocate and lobby for tax incentives to enhance the attractiveness of the ownership under MREIF mortgage program. These incentives could take various forms, such as exemptions on capital gains tax up to a specified limit in the event of an outright sale or allowing mortgage interest payments to be deducted from a homeowner’s taxable income based on their tax bracket. Implementing these incentives would improve the financial viability of homeownership under MREIF, increasing housing demand. In turn, this demand growth would encourage developers to expand supply, ultimately stimulating the broader housing and construction sectors.

By implementing these recommendations based on the rent vs. own analysis, the EFIs can create a sustainable homeownership cycle, where:

- A first-time buyer purchases a home under the MREIF program.

- Over time, the homeowner builds equity through appreciation and loan repayment.

- After five years, the homeowner can apply their accumulated equity toward purchasing a larger home.

- The process repeats, allowing homeowners to upgrade their housing as their financial capacity and family size grow, while new qualified buyers enter the MREIF housing market by acquiring/assuming the homes vacated by the initial owners.

This structured approach ensures that EFIs not only facilitates homeownership but also promotes long-term housing stability. By providing a clear path for homeowners to progress naturally from starter homes to larger residences without undue financial difficulty, the MREIF can sustain continuous housing demand, stimulate growth in the housing sector, and play a crucial role in addressing the national housing deficit.

Credit: Ketut-Subi-Yanto | pexels.com

Conclusion

The point here is simple: if your annual rent, when broken down monthly, is equal to or even higher than what a monthly mortgage repayment would cost in the same area, then yes, renting is a waste of both time and money. However, one must consider (i) whether there’s a suitable property available for purchase in the desired location; and (ii) whether the prospective buyer even qualifies for a mortgage in the first place. Without both conditions, the argument that renting is a waste becomes far less convincing.

This is where the role of the EFIs becomes critical. They must take this reality into account in structuring and rolling out mortgage products that are not only competitive with renting but also accessible to qualified renters looking to make the transition to homeownership.

By implementing policies that enhance affordability, flexibility, and long-term wealth creation, EFIs can position ownership under the MREIF mortgage as a viable pathway to sustainable homeownership. A well-structured housing finance system must account for key variables such as interest rates, equity appreciation, tax incentives, and rental price dynamics to ensure that homeownership remains an economically sound decision for prospective buyers.

Ultimately, whether an individual chooses to rent or own will depend on their unique financial circumstances, risk tolerance, and long-term housing goals. However, for EFIs to fulfill their mission as drivers of the MREIF scheme, they must continually evolve to offer homeownership models that align with economic realities, incentivize market participation, and drive housing sector growth.

END.

Disclaimer

This publication is for informational purposes only and does not constitute legal, financial, or investment advice. While every effort has been made to ensure accuracy, readers should seek professional counsel before making real estate or financial decisions. The opinions expressed herein are those of the author and do not necessarily reflect the views of Boldmen Bridgewaters Advisory or any affiliated institutions. Neither the author nor the publisher assumes any liability for decisions made based on this analysis.

About the Author

Da-tonye Bright Agborubere is the Lead Solicitor and Head of Research for Boldmen Bridgewaters Advisory–a boutique corporate/commercial real estate firm based in the city of Awka, Anambra State, Nigeria. With a strong background in real estate finance, property law, investment analysis, and strategy, he provides expert advisory services on structured real estate transactions, mortgage financing, and housing policy development.

His work focuses on market analysis, regulatory frameworks, and investment modeling to support institutional and private sector stakeholders in navigating the evolving Nigerian real estate landscape. Through rigorous research and strategic insights, he contributes to advancing sustainable homeownership models and innovative financing solutions in the industry.

Join The Discussion